CCUS: A Key Technology Linking Carbon Neutrality and the Circular Economy

2025.08.28

🔍 To address climate change, nations are ramping up renewable energy adoption and enhancing energy efficiency. However, in sectors such as steel, cement, and petrochemicals—where CO₂ emissions are an inevitable byproduct—traditional reduction measures face clear limits. CCUS (Carbon Capture, Utilization, and Storage) has emerged as a crucial technology to bridge this gap.

In this article, we examine the concept and importance of CCUS, review policy and market developments across the EU, U.S., Japan, and Korea, and highlight the opportunities and implications that lie ahead.

What is CCUS?

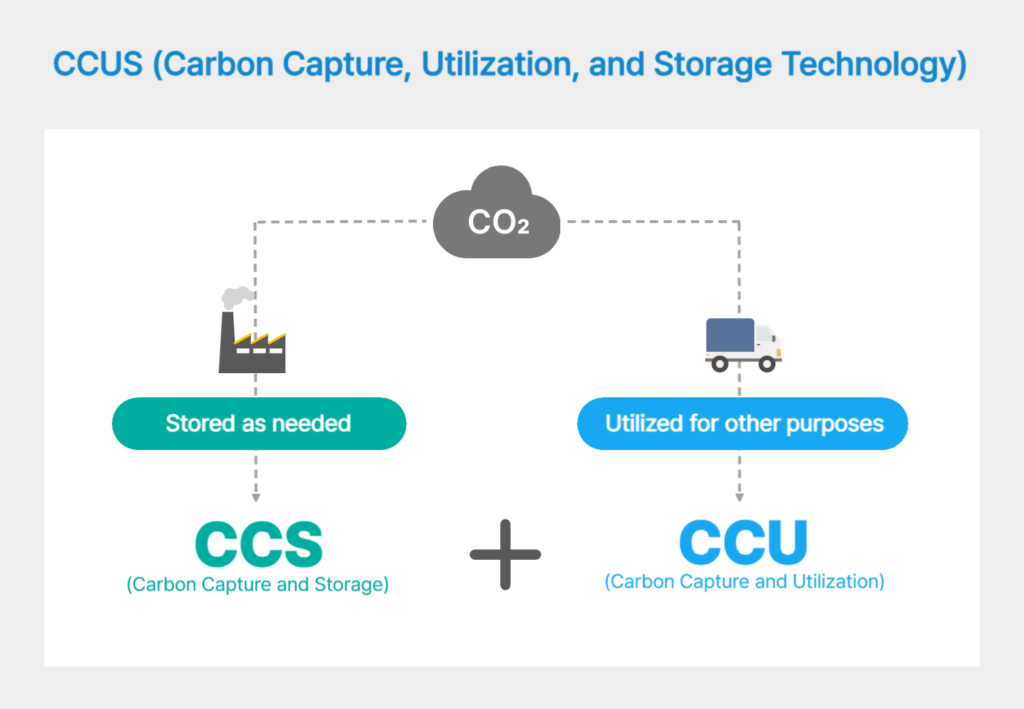

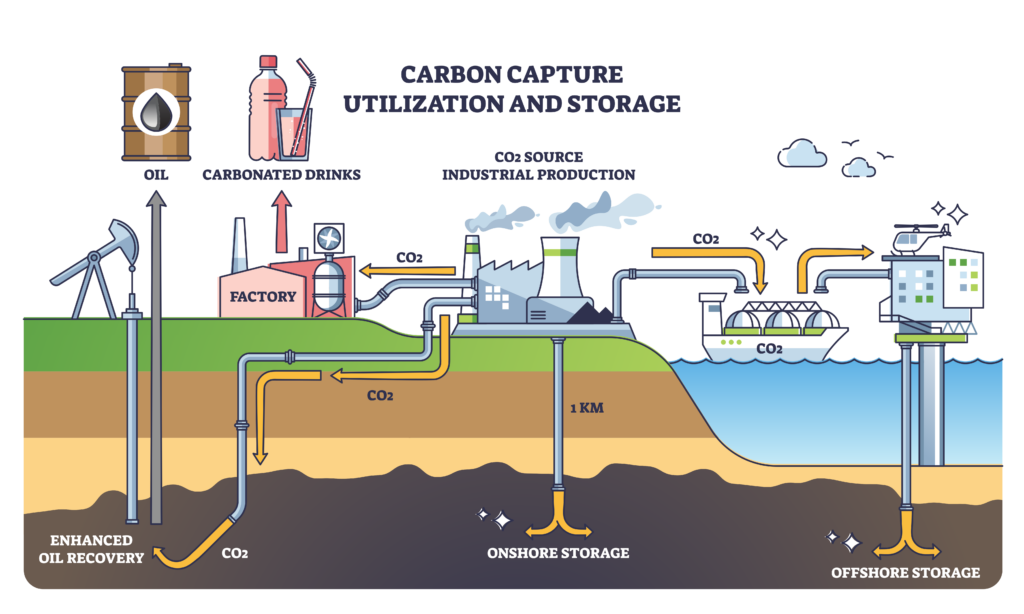

CCUS (Carbon Capture, Utilization, and Storage) is an integrated technology that captures CO₂ emissions from large-scale industrial facilities and power plants, reuses part of it as a resource, and stores the remainder in geological formations or marine environments for the long term. By combining CCS (Carbon Capture and Storage) and CCU (Carbon Capture and Utilization), it unites the strengths of both approaches.

CCS involves permanently storing captured CO₂ in underground geological formations. Commercially demonstrated since the 1990s, it has been recognized as a key carbon reduction technology, particularly effective in hard-to-abate industries such as steel and cement. However, concerns over limited storage capacity and potential leakage risks from natural events like earthquakes have highlighted its limitations.

To address these challenges, CCU emerged. CCU transforms captured CO₂ into valuable industrial resources such as chemical feedstocks, synthetic fuels, and construction materials. This not only reduces the pressure of securing storage sites but also turns CO₂ into an economic asset, positioning it as a practical alternative to CCS.

Consequently, CCUS has evolved into a comprehensive solution that integrates CCS and CCU—overcoming storage constraints and safety concerns while enabling a more sustainable path for industrial transformation.

Global Policies and Market Trends

CCUS is increasingly recognized worldwide as a critical technology for directly reducing unavoidable CO₂ emissions, spurring active research and investment.

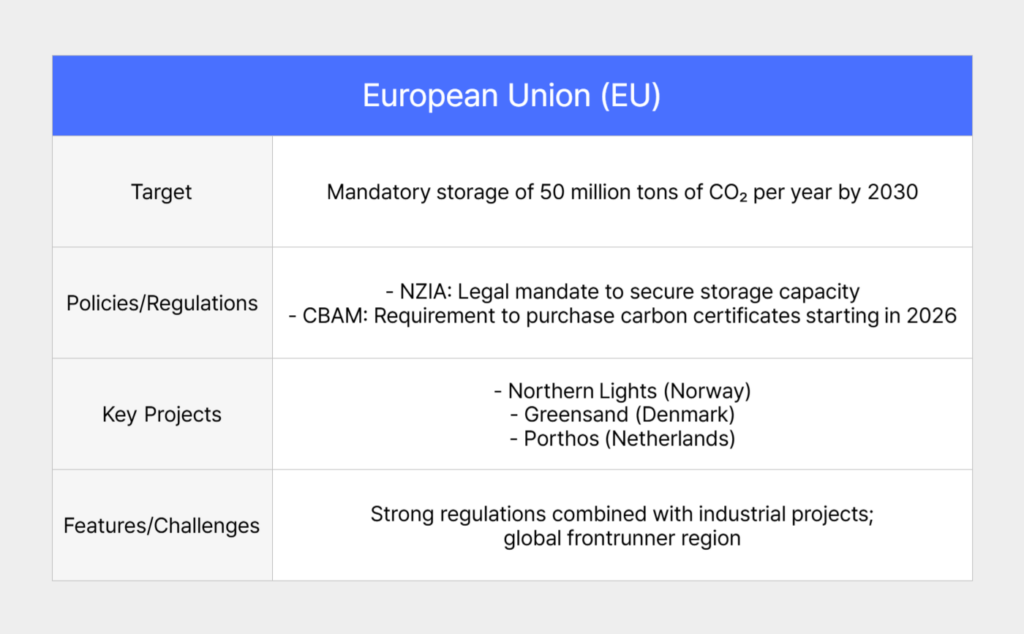

1) Europian Union – Expanding CCUS with Strong Regulation and Storage Requirements

The EU has mandated a significant expansion of CO₂ storage capacity by 2030, providing a strong foundation for CCUS market growth.

Under the Net-Zero Industry Act (NZIA), companies must secure an annual CO₂ storage capacity of 50 million tons by 2030, sending a clear signal of demand for CCUS. In addition, starting in 2026, the Carbon Border Adjustment Mechanism (CBAM) will require importers of carbon-intensive products—including steel, cement, aluminum, fertilizers, electricity, and hydrogen—to purchase carbon certificates. During the transition period from 2023 to 2025, importers must report emissions quarterly, adding pressure on exporters to adopt CCUS and low-carbon technologies.

Several large-scale projects are already in motion. Norway’s Northern Lights project is set to begin commercial operations in 2025, storing CO₂ transported by ship from across Europe in the North Sea. Denmark’s Greensand project, the EU’s first commercial-scale storage initiative, plans to expand capacity to 8 million tons per year by 2030. The Netherlands’ Porthos project is developing infrastructure to transport CO₂ from the Rotterdam industrial cluster through offshore pipelines for storage in the North Sea.

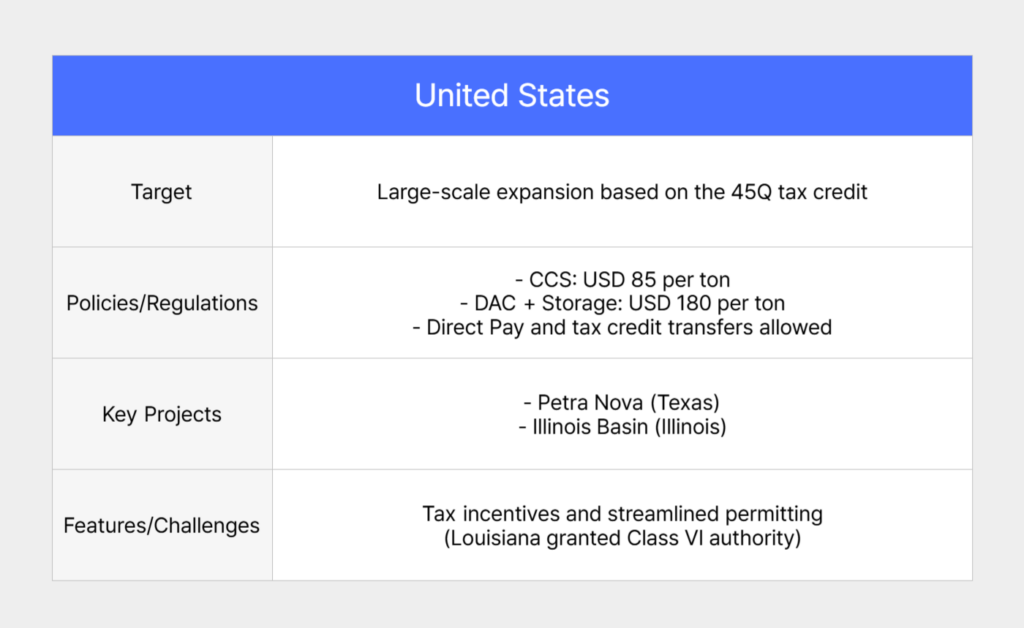

2) United States – Driving Investment with Tax Incentives and Regulatory Easing

The United States is accelerating CCUS deployment by combining financial support with streamlined regulation. At the center is the 45Q tax credit, which provides up to USD 85 per ton of CO₂ stored in geological formations and up to USD 180 per ton for projects that combine Direct Air Capture (DAC) with storage. These credits can be monetized through cash refunds or transfers, making them highly attractive to private investors.

Regulatory improvements are also helping. Since February 2024, Louisiana has held authority over Class VI permits for CO₂ storage, significantly speeding up project approvals. This demonstrates how federal support and state-level deregulation are working hand in hand.

The U.S. also hosts several flagship projects. The Petra Nova project in Texas captures CO₂ from a coal-fired power plant and uses it for Enhanced Oil Recovery (EOR). In Illinois, the Illinois Basin project stores CO₂ from bioethanol plants in geological formations, serving as a large-scale demonstration.

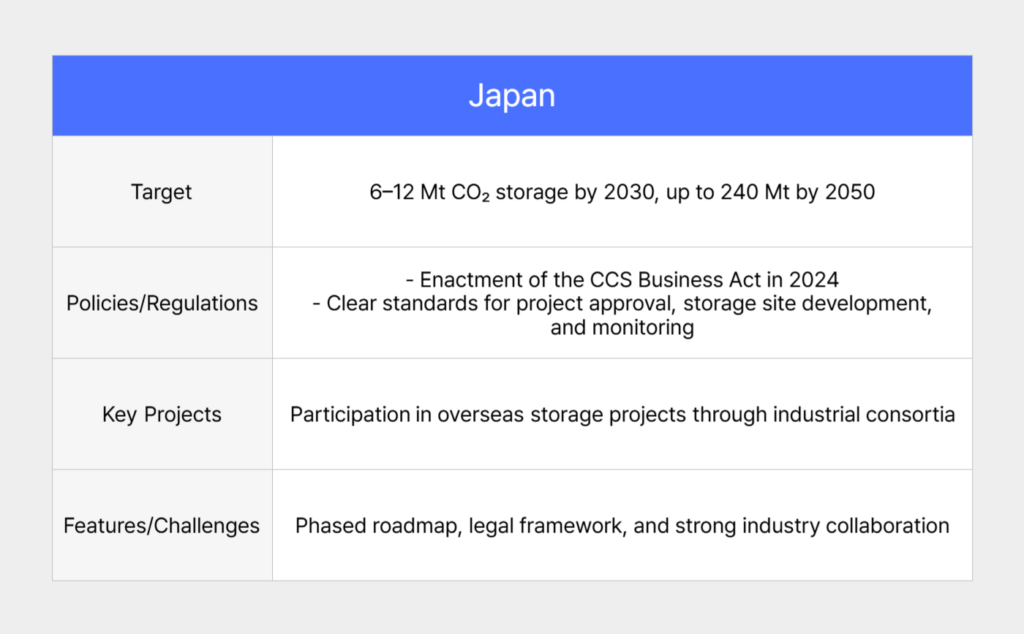

3) Japan – Step-by-Step Commercialization Based on Roadmaps

Japan is advancing CCUS commercialization through a phased roadmap. The government has set a target of storing 6 to 12 million tons of CO₂ annually by 2030 and projects expansion to as much as 240 million tons by 2050, balancing short-term feasibility with long-term growth potential.

The legal framework has also been strengthened. In June 2024, the Ministry of Economy, Trade and Industry (METI) enacted the CCS Business Act, which clearly defines procedures for project approvals, storage site development, and long-term monitoring standards. This provides a stable foundation for investment and business development.

Japanese industries in oil, gas, power, and chemicals are forming consortia to participate in overseas storage projects. This approach not only increases domestic storage capacity but also positions Japan to secure leadership in the global CCUS value chain through international cooperation and technology exchange.

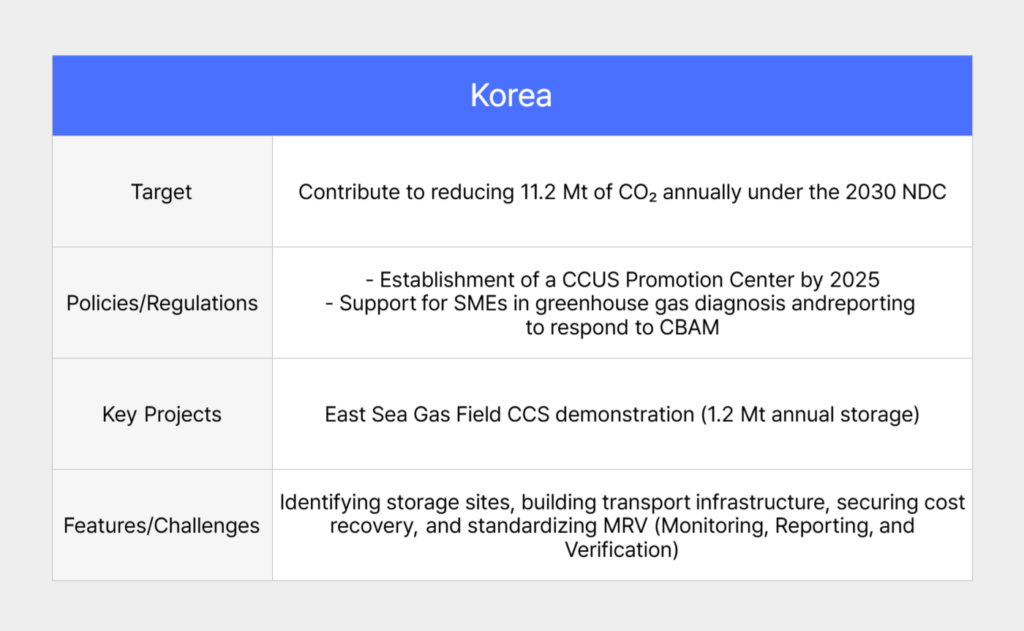

4) Korea – 2030 Reduction Target and East Sea Gas Field Demonstration

Korea has pledged to cut 11.2 million tons of CO₂ annually through CCUS under its 2030 Nationally Determined Contribution (NDC), highlighting the technology’s central role in achieving carbon neutrality.

A key milestone is the East Sea Gas Field CCS demonstration project, which is designed to store about 1.2 million tons of CO₂ each year in subsea formations. This marks the country’s first commercial-scale CCS pilot.

Policy support is also expanding. By 2025, the government plans to establish a CCUS Promotion Center to drive technology development and infrastructure expansion. It is also preparing greenhouse gas monitoring and reporting systems for small and medium-sized enterprises (SMEs) to help them comply with the Carbon Border Adjustment Mechanism (CBAM).

Despite these efforts, challenges remain. Korea must still identify suitable offshore storage sites, build CO₂ transport infrastructure, establish viable economic models, and standardize MRV (Monitoring, Reporting, and Verification) systems.

What Role Does CCUS Play in the Clean Energy Transition?

CCUS enables the continued operation of existing power plants and industrial facilities by equipping them with capture systems. It is particularly effective in cutting emissions from hard-to-abate sectors such as cement, steel, and chemicals. The technology also supports the low-cost production of low-carbon hydrogen, accelerating decarbonization across the wider energy system. In addition, by directly removing CO₂ from the atmosphere, CCUS helps offset residual emissions.

For these reasons, CCUS is widely viewed as a cornerstone of the clean energy transition. The International Energy Agency (IEA) emphasizes its importance, noting that as of 2024, global CCUS facilities capture and store around 51 million tons of CO₂ each year. With additional projects under construction or in planning, capacity is projected to exceed 400 million tons by 2030—evidence of the rapid growth that lies ahead.

The Path to Carbon Neutrality: Heesung Catalysts’ Challenge Toward CCUS Commercialization

The global policies, market trends, and energy transition roles outlined above demonstrate that CCUS is indispensable for achieving carbon neutrality. Countries are accelerating commercialization through regulations, incentives, and legal frameworks, developments that also carry significant implications for domestic industries.

In step with this global movement, Heesung Catalysts is making consistent investments in foundational R&D to advance CCUS commercialization. Leveraging its expertise in environmental catalysts, emission-reduction solutions, and eco-friendly materials, the company is delivering practical answers for hard-to-abate sectors such as steel, cement, and chemicals.

Looking ahead, Heesung Catalysts will continue to foster innovation and broaden its green business portfolio, offering a diverse range of solutions aligned with the global pursuit of carbon neutrality. The company is dedicated to being a trusted partner on the journey toward a cleaner, more sustainable future.